LLC default tax classification refers to the way the IRS automatically classifies a limited liability company (LLC) for tax purposes following application for an Employer Identification Number (EIN). By default, the IRS taxes an LLC according to the number of members it has, but the LLC can change its tax status by electing another recognized tax classification.

Tax Classifications for LLCs

Every new LLC owner, also known as member, is required to choose a tax classification. Unlike some other business structures, LLCs can be taxed in several different ways. Since the Internal Revenue Code does not include specific provisions for taxing LLCs, the IRS requires them to choose recognized business structures for tax purposes. However, it is important to note that LLCs will remain as LLCs regardless of their tax classifications. There are three main tax classifications for LLCs to choose from:

- Disregarded entity

- Partnership

- Corporation (C corporation or S corporation)

While some of these tax classifications occur by default, others require filing with the IRS. When it comes to tax classification, there is no one-size-fits-all option. In order to make the right decision, an LLC and its members have to take a number of factors into consideration, including:

- Business size

- Goals of members

- Financial plans

Types of LLC Tax Classifications

Disregarded Entity

An LLC that chooses to be a disregarded entity will be taxed as a pass-through entity. This means that it will be considered a sole proprietorship that files Schedule C. As such, the LLC and its owner will be regarded as one and the same entity for tax purposes. In this case, the owner will pay taxes as a self-employed person by filing the same self-employment tax forms as individuals who freelance or conduct business under their own names.

Partnership

An LLC that has multiple members can choose to be taxed as a partnership. Similar to those classified as disregarded entities, an LLC that is taxed as a partnership is considered a pass-through entity, meaning that its owners are taxed individually for profits and losses. It is required to file IRS Form 1065 with a Schedule K1 for each member.

When an LLC is classified as a partnership, its owners will still be taxed for its profits even if they do not actually receive their portions of the profits (i.e. profits are left in the company’s bank account). However, unlike an LLC with disregarded entity classification, an LLC with partnership classification is required to report to the IRS despite not being the subject of taxation. In addition, it must prepare certain forms and documents to help its owners file their tax returns.

Corporation

All LLCs, including single-member entities, can elect corporation tax classification. Under the corporation classification, both the LLC and its owner are required to report certain information. If an LLC opts for C corporation tax classification, it will be taxed as a corporation. The company is subject to taxation, and its owners must pay personal income tax on the dividends they receive, resulting in double taxation. A C corporation is required to file its tax returns on IRS Form 1120, while its owners report their incomes on W-2s.

If an LLC chooses to be taxed as an S corporation, it does not have to pay federal taxes on its profits. Instead, the profits will pass through to its owners, who will in turn report them on their individual tax returns. Another benefit of choosing S corporation classification is that it allows an LLC’s owners to use its losses to offset the income received from other sources. However, owners are required to pay self-employment tax on their earnings, which is 15.3 percent of their net incomes after expenses.

Creating an LLC Tax Classification

If you fail to elect a tax classification for your LLC, the IRS will automatically assign your LLC a tax classification based the number of members it has. If you wish to choose a different tax classification, you are required to file IRS Form 8832.

In most cases, you must file this form within 75 days of your LLC’s formation. If you miss the deadline, you are required to submit the form within 75 days of the following tax year. The IRS will accept late elections under limited circumstances.

Fortunately, if you miss the 75 day deadline, you are able to still file the form 8832. There are two main provisions to consider:

1. Late classification relief sought under Revenue Procedure 2009-41 permits relief for certain late entity classification elections and extends the period for making a late entity classification election to three years and 75 days after the requested effective date of such election.

2. Relief for a late change of entity classification election sought under Revenue Procedure 2010-32 provides relief to certain foreign eligible entities that made erroneous entity classification elections (check-the-box elections) based on a mistaken understanding of the number of owners as of the effective date of the election.

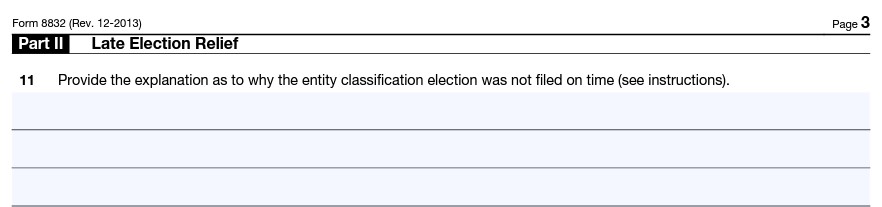

Part 2, Section 11 asks to Provide the explanation as to why the entity classification was not filed on time.

A suitable response would be for this section might be:

“Company’s owner failed to file the 8832 form within the first 75 days of formation. Please be advised that no tax deadlines have occurred up to this point.”.

Since the tax status of your LLC can usually be changed only once in five years, it is advisable that you consult a professional advisor before you file Form 8832.

0 Comments