The practice of seller financing goes by many names, including purchase-money mortgages and owner financing. But in its simplest terms, it describes a form of real estate lending transaction in which a property owner also serves as a mortgage lender. This unique situation in the home selling process eliminates the need for a financial institution to handle financing agreements and negotiations.

What Is Seller Financing?

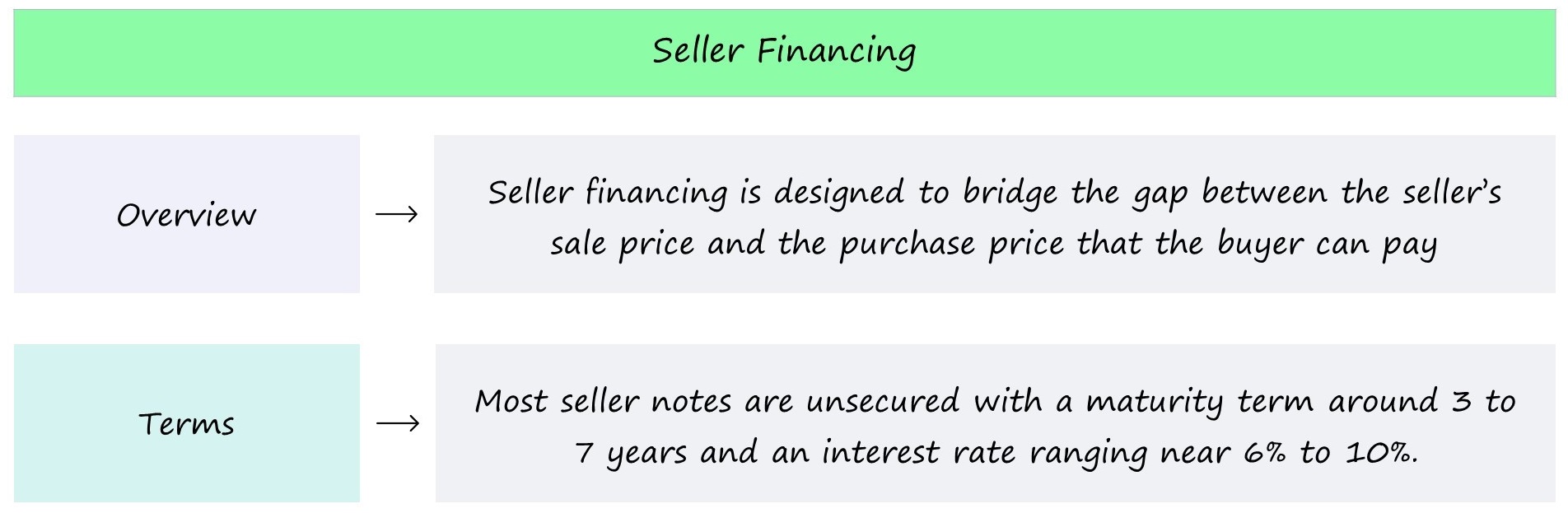

Seller financing is a type of real estate agreement that allows the buyer to pay the seller in installments rather than using a traditional mortgage from a bank, credit union or other financial institution. A seller financing agreement functions along similar lines as a mortgage loan, except that it cuts out the middleman and allows the home seller to own and oversee the debt instead of a traditional lender.

If you choose to opt for a purchase-money mortgage (a mortgage that is issued to a home buyer directly by a property seller), then the seller will provide financing and handle the mortgage process, during which you will enter into a mortgage with the seller instead of a corporate lender. Also sometimes referred to as owner financing or purchase-money mortgages, seller financing’s advantages include no minimum down payment, homeownership access for those with poor credit and fewer regulations. But these same upsides can quickly become disadvantages as well.

Common Types Of Seller Financing Agreements

Certain home buyers may find these options (which may provide more opportunities to finance a home purchase and may even come without a credit check attached) attractive, especially low-income or first-time home buyers. Be advised, though: Some seller financing offers may function more like rental agreements than traditional mortgages, and offer unfavorable loan terms that offset any initial benefits to be had. As with any form of mortgage agreement and legally binding real estate contract, it’s important to do your research, and consult with a qualified professional upfront.

Let’s look at the most common types of seller financing arrangements:

- Land contracts: A land contract is an agreement to purchase a piece of real estate that involves buyers borrowing money from the real estate owner until the purchase price is paid in full, rather than from a bank, credit union or financial institution. Land contracts typically work in a unique fashion where a balloon payment, or lump sum, comes at the end of the repayment period after the repayment plan is negotiated between the two parties.

- Assumable mortgage: An assumable mortgage is a type of home financing in which buyers are given the opportunity to purchase a home by assuming responsibility for and taking over the seller’s current mortgage (especially if it’s charged at a lower interest rate).

- Lease purchase: Also known as a rent-to-own contract, a lease purchase agreement speaks to a form of agreement under which renters pay sellers an option fee at an agreed-upon purchase price that gives the renter the exclusive lease option to purchase the property at a later date.

- Land loans: A land loan is used to facilitate and finance the purchase of a plot of land for later use for residential or business purposes.

- Holding mortgage: Under a holding mortgage agreement, a homeowner agrees to serve as a lender for the home buyer, and provides a loan for the purchase, which the buyer repays by making monthly payments to the seller. The seller continues to hold the property’s title until full loan repayment has been made by the buyer.

Seller Financing Advantages For Sellers

Seller financing may prove a good option for those wishing to lend money. Select upsides associated with providing it include:

- Ability to save on closing costs

- Can produce significant capital gains tax savings over time

- Faster time to sale, and ability to sell your property as-is without the need for repairs

- Released from property tax, homeowners insurance and various maintenance expenses

- Option to sell the promissory note to an investor

Seller Financing Advantages For Buyers

Buyers may also enjoy several benefits should they elect to buy an owner-financed home, such as:

- Greater access to financing opportunities, especially for low-income buyers

- Lower expenses associated with closing costs

- More flexible agreement terms

- Potential for no PMI premiums

- More accessible for those with poor credit

Disadvantages Of Seller Financing

As alluded to above, seller financing is not without its potential drawbacks as well. Items you may wish to keep in mind as you consider whether to pursue this form of real estate financing option are as follows:

- Fewer regulations that protect home buyers

- Buyers still vulnerable to foreclosure if seller doesn’t make mortgage payments to senior financing

- No home inspection/PMI may result in buyer paying too much for the property

- Higher interest rates and bigger down payment required

- Seller faces risks if the borrower defaults on payment

Seller Financing FAQs

As previously noted, there are pros and cons to weigh when debating whether or not to enter into a seller financing agreement. Read on to find answers to several frequently asked questions (FAQs) associated with this form of real estate transaction.

What is the difference between a purchase-money mortgage, seller financing and owner financing?

These terms are all one and the same – a purchase money mortgage is a loan that’s made to a home buyer by the property seller. This process may also be referred to as owner financing.

Is seller financing a good idea?

The answer is entirely dependent on your personal situation and needs. As a home buyer, seller financing may make more lending opportunities available to you, just as it may present an added opportunity for financial benefit to home sellers. However, there are advantages and disadvantages to the practice as well, as outlined above.

Who holds the title in seller financing?

Under the terms of seller financing, the property owner (the home seller) retains the title to the home as a form of leverage until the mortgage has been paid off in full.

The Bottom Line

Seller financing presents upsides and downsides to home buyers and sellers alike. With these agreements, purchasers with lower credit scores or incomes may be able to obtain loans that they could not have been approved for otherwise.

At the same time, the interest rate that a seller may charge can often exceed that charged by a traditional mortgage lender. So, while seller financing can open up more possibilities to aspiring home buyers when it comes to real estate transactions (and potentially provide home sellers with added investment opportunities and tax savings), it won’t make sense to utilize in every case.

To learn more about seller financing and whether it’s ideal for you, research and consult with a qualified professional such as a real estate attorney before entering into an agreement.

Review the terms and conditions of any owner financing contract, too – they may vary greatly between agreements as well. Crunch the numbers to see if upfront savings on a property purchase made in this fashion may cost you more in the end.

0 Comments